Issues in this category: when the charged amount is larger than the authorization amount on a card, when there is no valid authorization or when the authorization approval has expired.

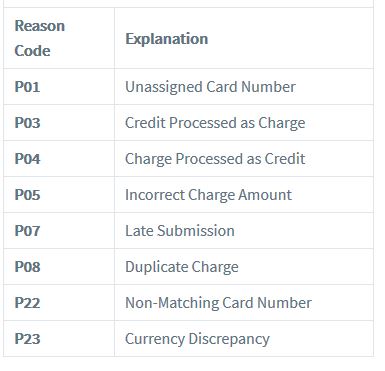

Issues in this category: when a card number hasn’t been assigned, issues with a credit being processed as a charge (or a charge being processed as a credit), when the wrong amount is charged or when there is an inconsistency in the currencies used.

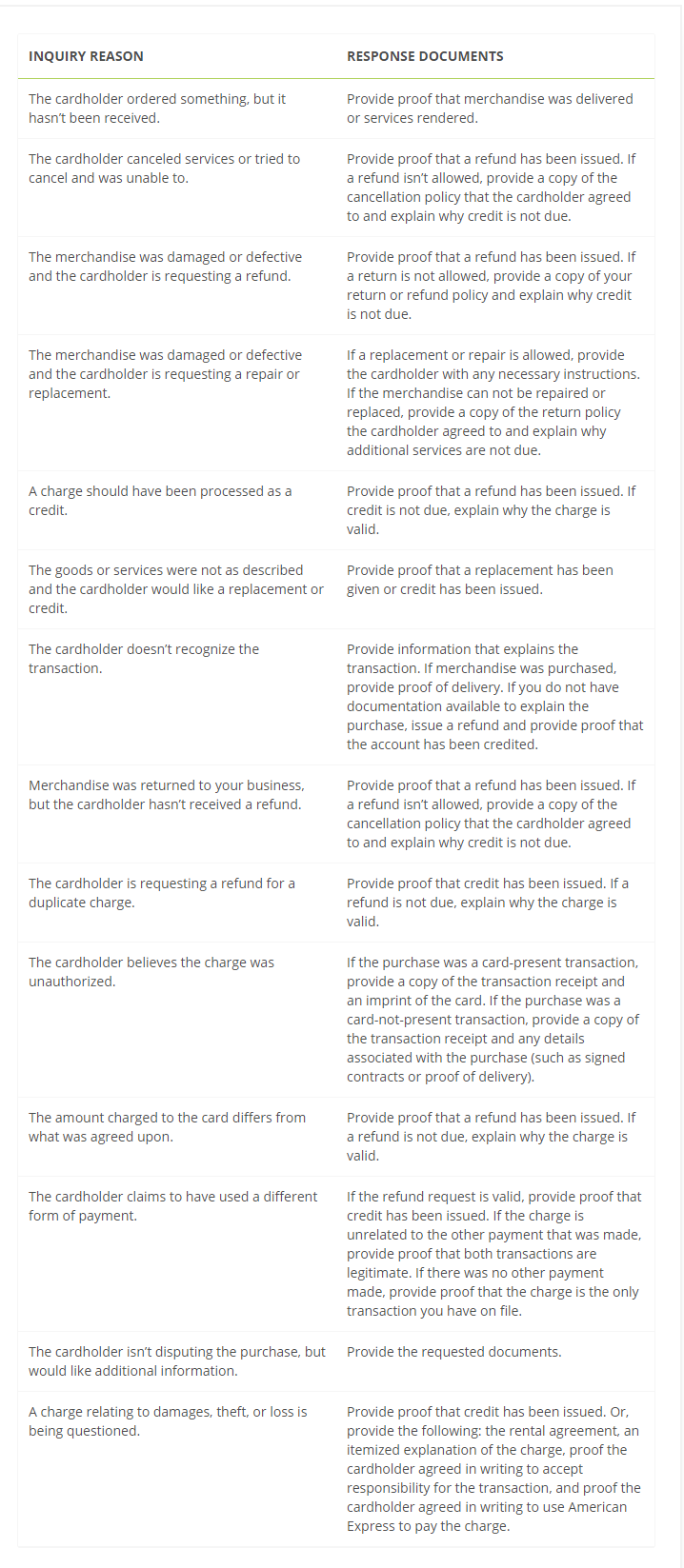

Issues in this category: cards not being processed, merchandise or services being returned, refused, not as described, damaged, canceled or partially received.

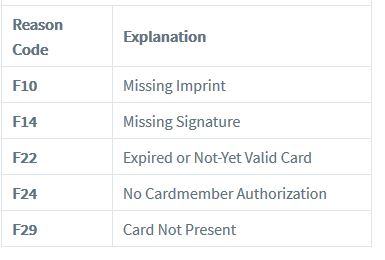

Issues in this category: missing imprints, missing signatures, expired or invalid cards, when cards aren’t present during a purchase or when there is no cardholder authorization.