Issues in this category: when the charged amount is larger than the authorization amount on a card, when there is no valid authorization or when the authorization approval has expired.

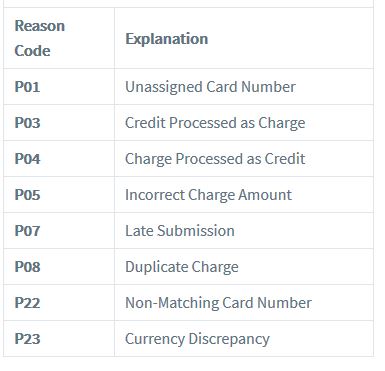

Issues in this category: when a card number hasn’t been assigned, issues with a credit being processed as a charge (or a charge being processed as a credit), when the wrong amount is charged or when there is an inconsistency in the currencies used.

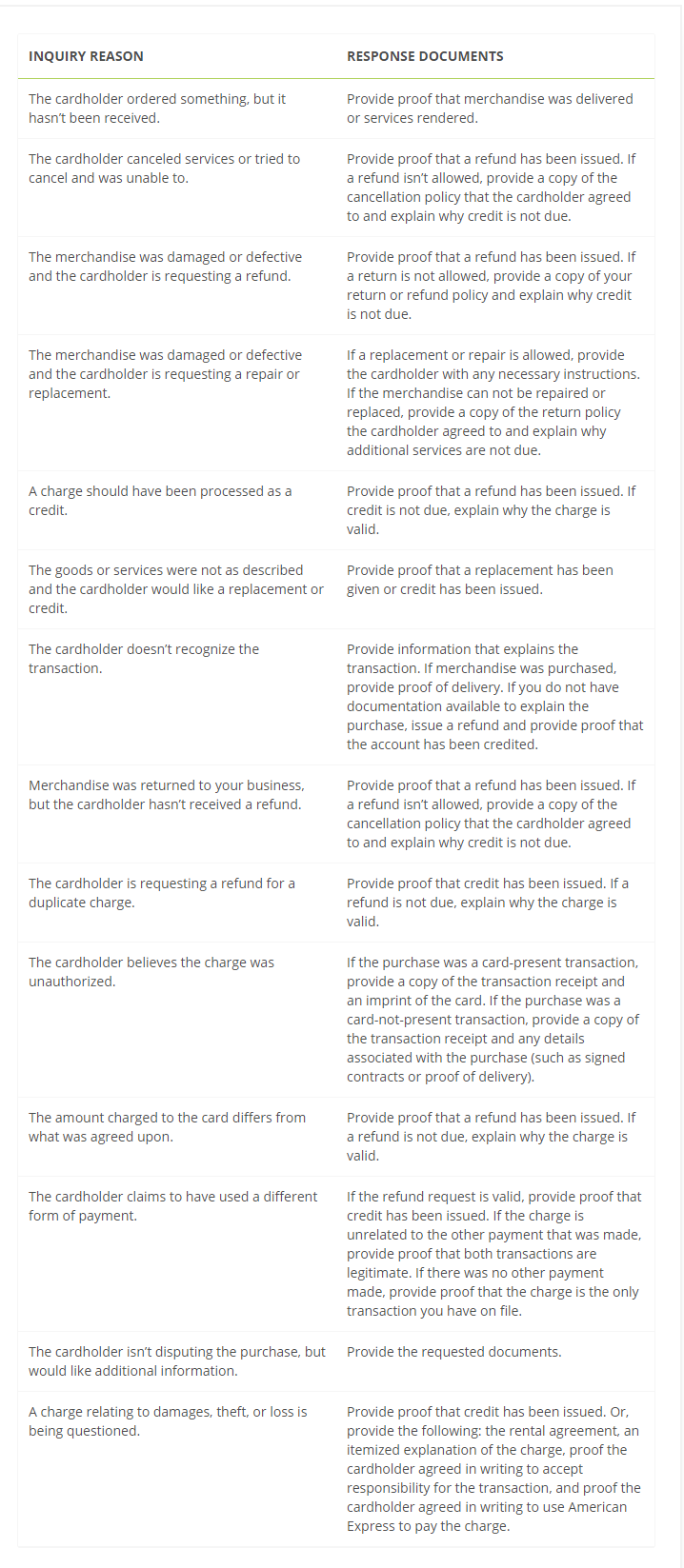

Issues in this category: cards not being processed, merchandise or services being returned, refused, not as described, damaged, canceled or partially received.

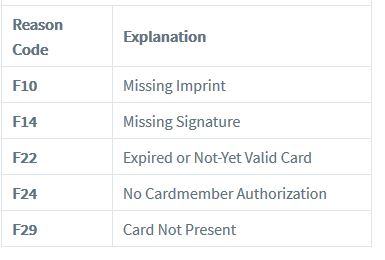

Issues in this category: missing imprints, missing signatures, expired or invalid cards, when cards aren’t present during a purchase or when there is no cardholder authorization.

9 Comments

Learn everything you need to know about managing disputes, including how the process works and tips for avoiding disputes in the first place. A dispute occurs when a Card Member contacts American Express to question a charge on their statement that they don’t recognise. A chargeback occurs when, after investigation of the dispute, we debit your account for the amount of the disputed transaction and credit the Card Member with this amount. There are simple steps you can take to minimise the chances of a dispute and chargeback happening.

Awesome post! Keep up the great work! 🙂

Great content! Super high-quality! Keep it up! 🙂

Thank you!

Very shortly this web page will be famous amid all blogging viewers, due to it’s good articles or reviews

Thank you for sharing your info. I truly appreciate your efforts

and I will be waiting for your next write ups thanks once again.

I’m excited to uncover this great site. I wanted to thank you for your time for this

particularly wonderful read!! I definitely appreciated every bit of it and

I have you book-marked to check out new information on your blog.

Wow, superb blog layout! How long have you been blogging for?

you make blogging look easy. The overall look of your website is wonderful, let alone the content!

I like the valuable information you provide to your articles.

I’ll bookmark your blog and test once more right here frequently.

I am slightly certain I’ll be informed a lot of new stuff proper here!

Good luck for the following!

Comments are closed for this article!